Abacus is a Bayesian MMM library built on PyMC and PyTensor. It provides PanelMMM for multi-market panel modelling, structured YAML-driven configuration, a staged pipeline runner, and budget optimisation — all designed for reproducible, production-grade MMM workflows.

For a real end-to-end verification path, use the repo smoke target:

make smoke_mmm

If you are working on the repo itself, the main local verification commands

are:

make testmake verify_local

make verify_package

Runtime defaults for restricted environments

Some local runs need writable cache directories. If you hit PyTensor compiledir

or cache-permission issues, export the same defaults used by the repo

verification scripts:

This page shows the fastest direct path from a pandas dataset to a fitted

PanelMMM.

If you have not prepared your dataset yet, read

Data Preparation first.

Load a dataset

The repository includes bundled demo datasets under data/demo/. The

timeseries bundle is the simplest starting point because it has no extra panel

dimensions.

The bundled demo config at data/demo/timeseries/config.yml is a working

starting point. It already points to a combined dataset with

data.dataset_path.

If you rely on data.dataset_path, either split the combined dataset in Python

before fitting, or load it once in Python and pass the same X and y into

both build_mmm_from_yaml(...) and fit(...).

Optional top-level YAML blocks

The builder recognises several optional top-level sections in addition to

data, target, and media.

Key

Purpose

dimensions

Panel-dimension columns such as geo or brand

scaling

Optional scaling rules for target and channels

effects

Additive effects to attach before model build

priors

Model-level priors passed into PanelMMM

fit

Sampler defaults used by the runner or by Python overrides

holidays

Holiday/event configuration applied before build

original_scale_vars

Add original-scale deterministic variables after build

inference_data

Attach existing inference data if the file exists

calibration

Apply calibration steps after the model is built

Override config values from Python

Use model_kwargs when you want to keep most settings in YAML but override a

subset from Python.

For example, you can override the fit config for a lighter quickstart run:

model_kwargs takes precedence over the YAML defaults.

Next steps

Read Quickstart: Pipeline Runner if you want staged

artefacts and manifests instead of an in-memory fit only.

Read Data Preparation for dataset column and

layout requirements.

Quickstart: Pipeline Runner

Use the pipeline runner when you want a full staged run instead of only an

in-memory model fit.

The runner writes:

a run manifest

copied and resolved config files

fitted model artefacts

posterior predictive assessment outputs

decomposition, diagnostics, and response-curve artefacts

Fastest first run: bundled demo

From the repository root, the quickest way to see a real structured run is the

demo launcher:

python3 runme.py --demo timeseries

Other bundled demos are:

geo_panel

geo_brand_panel

List them explicitly with:

python3 runme.py --list-demos

runme.py is a convenience wrapper around the structured pipeline. It resolves

the demo config under data/demo/<demo_name>/config.yml and runs the pipeline

for you.

This section explains how to prepare X and y for PanelMMM.

It covers the required columns, how panel rows are organised when you use

dims, and how Abacus scales channels and the target before fitting.

Pages

Input Data Requirements — Required X and y

inputs, column roles, alignment rules, and common input errors.

Panel Data Layout — How to structure rows for no

panel dims, one dim such as geo, or multiple dims such as geo and

brand.

Scaling and Preprocessing — What Abacus

scales automatically, how Scaling works, and what to preprocess yourself.

y as a pandas.Series named target_column, or a one-dimensional NumPy

array of the same length as X

X must contain the date column, all media columns, and any configured

control_columns or dims columns. y carries only the target values.

Role

Where it must be present

Required

Notes

date_column

X

Yes

Normalise to datetimes or parseable date strings.

channel_columns

X

Yes

Every listed channel column must exist in X.

target_column

y

Yes

y.name should match target_column.

control_columns

X

No

If configured, every listed control column must exist in X.

dims

X

No

One column per configured panel dimension, such as geo or brand.

X and y

When you call fit(X, y) or build_model(X, y):

Keep the target out of X.

Keep X and y row-aligned.

If both are pandas objects, keep the same index on both. The shared

regression builder checks index equality before fitting.

If you pass y as a NumPy array, its length must match len(X).

For panel models, each date_column + dims combination must appear

exactly once. Duplicate rows are rejected.

Abacus uses target_column as the target name throughout the panel reshape.

If y is a Series, its name must match target_column.

Date column

date_column is required in X.

Abacus expects calendar dates, not integer date codes. In practice:

Use datetime64[ns] where possible.

Parse string dates with pd.to_datetime(...) before fitting when you use the

Python API.

Do not rely on numeric date values such as 0, 1, 2. Pandas can interpret

them as offsets from the Unix epoch, which is usually not what you want.

The YAML builder normalises X[date_column] with pd.to_datetime(...) after

loading the dataset. Direct Python use does not add an equivalent preprocessing

step for you.

Channel columns

channel_columns is a required constructor argument and must be a non-empty

list.

Each listed channel:

must be present in X

must be fully observed for every row you pass into fit or posterior

prediction; Abacus does not silently convert missing channel values to zero

should represent the raw media variable that you want the adstock and

saturation transformations to consume

Target column

target_column names the dependent variable. It defaults to "y", but you can

set a different name such as "sales" or "conversions".

For direct Python use:

pass the target as y

name the Series with target_column

keep the target fully observed; missing target values are rejected rather

than zero-filled

For combined-file YAML or pipeline flows:

keep the target column in the source dataset

Abacus splits it out of the combined dataset before fitting

Control columns

control_columns is optional.

If you configure it, every listed control column must be present in X.

Controls stay in the design matrix as separate regressors; they are not part of

y.

Like channels, configured controls must be fully observed for every row passed

into fit or posterior prediction.

One tabular file containing both predictors and the target column

Pipeline runner with dataset_path

Same as above

Pipeline runner with x_path and y_path

Separate feature and target files; the runner extracts target_column from the target file

Abacus also has an internal alignment helper that can work with a MultiIndex

target Series indexed by [date_column, *dims], but that is mainly used in

fit-data rebuild and load flows. For normal fitting, keep y row-aligned with

X.

Missing date_column, channel, control, or dimension columns in X

Passing a ySeries whose name does not match target_column

Passing pandas X and y with different indexes

Passing a NumPy y with a different length from X

Passing duplicate panel rows or incomplete panel slices for a given date

Passing missing observed channel, control, or target values and expecting

Abacus to treat them as structural zeroes

Expecting the YAML builder or pipeline to find a target column that is not

present in the combined dataset

Leaving date values as numeric codes instead of normalising them first

Panel Data Layout

This page explains how PanelMMM expects panel rows to be organised in X.

For the column-level contract, see

Input Data Requirements.

What “panel” means in Abacus

In Abacus, a panel dataset repeats the same time axis across one or more

categorical dimensions in dims.

Each row represents:

one date_column value

one combination of dims values, if any

one set of channel and optional control values for that slice

With no extra panel dims, each date appears once. With dims=("geo",), each

date appears once per geo. With dims=("geo", "brand"), each date appears

once per geo + brand combination.

How dims work

Pass panel dimensions when you construct the model:

Abacus converts the pandas inputs into xarray datasets before building the

PyMC model.

Input role

Internal variable

xarray dims

X[channel_columns]

_channel

(date, *dims, channel)

X[control_columns]

_control

(date, *dims, control)

y

_target

(date, *dims)

The channel and control dimensions come from the configured column names,

not from row values.

Rectangularity, duplicates, and missing rows

Abacus builds xarray coordinates from the unique values it sees in:

date_column

each configured dimension column

the configured channel or control names

That has three practical consequences:

Keep the panel rectangular. Provide one row for every expected

date_column + dims combination.

Use explicit zeroes for structural no-spend or no-activity rows.

Keep declared channel, control, and target values observed within those rows.

Abacus rejects missing metric cells instead of silently converting them to

zeroes.

Do not use missing rows to mean “unknown”. Abacus validates panel shape

before reshape and raises an error if panel cells are missing.

Abacus also requires each date_column + dims combination to appear exactly

once. It does not aggregate duplicates for you. If you have duplicate rows,

deduplicate or aggregate them before fitting or posterior prediction.

Sorting and uniqueness

Sort your data before fitting:

first by date_column

then by each entry in dims

Abacus keeps dates in the order they appear in X, and time-varying features

infer time resolution from adjacent rows. A sorted dataset makes the time axis

deterministic and easier to reason about.

Also make sure that each date_column + dims combination appears once in the

prepared table, and that every expected panel slice is present for every date.

DataFrame versus MultiIndex handling

For normal fitting:

use a regular DataFrame for X

keep date_column and any dims as columns in that DataFrame

use a row-aligned Series for y

Abacus does have internal helpers that can align a MultiIndex target Series

indexed by [date_column, *dims], but that is not the main user-facing data

preparation pattern for fit().

Practical checklist

One row per date_column + dims combination

No duplicate rows for the same panel cell

Same set of dates for every panel slice

Explicit zeroes for true zero activity

No missing observed channel, control, or target values

Abacus scales channels and the target automatically before it builds the PyMC

graph for PanelMMM. This page explains what is scaled, how the Scaling

configuration works, and what you still need to preprocess yourself.

What Abacus scales automatically

Abacus computes scales from the reshaped xarray dataset immediately before model

construction.

Variable role

Automatic scaling

Notes

Target (y)

Yes

Divided by target_scale before the likelihood is built.

Channels (channel_columns)

Yes

Divided by channel_scale before adstock and saturation.

Controls (control_columns)

No

Controls enter the model on their original scale.

Date and dims columns

No

These define coordinates, not modelled numeric inputs.

Abacus stores the resulting scalers in the model as xarray data:

The YAML builder supports the same workflow through original_scale_vars:

original_scale_vars:- channel_contribution- y

original_scale_vars adds extra original-scale deterministic variables. It

does not change how the model is fit.

What Abacus does not preprocess for you

Abacus does not automatically:

scale controls

impute missing data in a domain-aware way

reinterpret missing observed channel, control, or target values as zeroes

sort the dataset for you

repair non-rectangular panel layouts

tolerate duplicate panel rows or incomplete panel slices

coerce Python-API dates to datetimes before fitting

Practical preprocessing advice

Before fitting:

normalise date_column with pd.to_datetime(...)

sort by date_column and then by dims

make panel gaps explicit instead of leaving missing rows

ensure every date_column + dims panel cell appears exactly once

impute missing observed channel, control, and target values before fitting or

posterior prediction instead of relying on implicit zero-fill

decide whether controls should be centred, standardised, log-transformed, or

otherwise prepared before they go into control_columns

choose scaling dims deliberately instead of relying on the default when you

use panel data

Common pitfalls

Expecting the default scaling to be per-group when it actually pools across

the configured panel dims

Adding date to VariableScaling.dims; Abacus rejects this

Forgetting that controls are left on their original scale

Treating VariableScaling.dims as dimensions to keep rather than dimensions

to reduce across

Assuming original_scale_vars changes fitting scale rather than adding extra

outputs

For the input table shape that scaling operates on, see

Panel Data Layout.

Model Specification

This section explains how PanelMMM is defined: the model structure, media

transforms, priors, panel dimensions, optional time variation, and calibration

hooks.

Pages

Model Overview - The actual PanelMMM mean structure,

scaled-space formulation, and optional components.

Adstock and Saturation - Supported media

transforms, their priors, and the adstock_first composition order.

Priors and Configuration - Default prior keys,

model_config, transform-prior overrides, and directional control priors.

Time-Varying Parameters - How

time_varying_intercept and time_varying_media use SoftPlusHSGP.

Seasonality and Trends - Built-in yearly

seasonality plus custom Fourier, trend, and event effects.

Panel Dimensions - How dims change the shape of the

data and parameters.

Calibration - Lift-test and cost-per-target calibration for

a built model.

Subsections of Model Specification

Model Overview

PanelMMM is an additive Bayesian marketing mix model built in PyMC. This page

describes the model structure that Abacus actually builds.

For input layout, see Data Preparation. For

individual configuration surfaces, see the other pages in this section.

Core structure

At fit time, Abacus builds the model mean in scaled target space as:

mu =

intercept_contribution

+ sum(channel_contribution over channel)

+ sum(control_contribution over control), if control_columns are configured

+ mundlak_contribution, if use_mundlak_cre=True

+ yearly_seasonality_contribution, if yearly_seasonality is enabled

+ any additional mu_effects

The observed target is then attached through the configured likelihood

distribution with mu=mu.

What is scaled and what is not

Before the PyMC graph is built:

channel data is scaled according to Scaling.channel

the target is scaled according to Scaling.target

controls are not scaled automatically

That means media and target priors operate on the model scale, not directly on

the original business units. For the scaling surface, see

Scaling and Preprocessing.

Model components

Component

Built when

Shape

intercept_contribution

Always

effectively ("date", *dims) in the model mean

channel_contribution

Always

("date", *dims, "channel")

control_contribution

control_columns is set

("date", *dims, "control")

mundlak_contribution

use_mundlak_cre=True

dims

yearly_seasonality_contribution

yearly_seasonality is set

("date", *dims)

Additional additive effects

You add entries to mu_effects

("date", *dims)

Abacus also adds total_media_contribution_original_scale automatically as a

deterministic on the original target scale.

Media path

Each channel column goes through the configured media transform path:

scale channel input

apply adstock and saturation through forward_pass(...)

optionally apply a time-varying media multiplier

contribute the result through channel_contribution

Use controls for non-media regressors such as price, macro indicators, or

competitor measures. Controls are configured with control_columns and use

gamma_control priors from model_config.

Panel dimensions

dims adds extra indexing axes such as geo, brand, or market.

With dims=("geo",), the model is indexed over date and geo. With

dims=("geo", "brand"), it is indexed over date, geo, and brand.

Abacus does not automatically add hierarchical pooling just because dims is

set. By default, parameters are indexed over the configured panel coordinates.

If you want hierarchical shrinkage across those coordinates, encode it in the

priors you pass to transforms or model_config.

PanelMMM requires one adstock transform and one saturation transform. Abacus

applies them inside the model graph rather than as a fixed preprocessing step.

Transform priors also appear in model_config under prefixed variable names.

For example:

adstock_alpha

adstock_lam

adstock_k

saturation_lam

saturation_beta

That means you can override transform priors centrally through the top-level priors

if you prefer. See Priors and Configuration.

Choose the composition order

adstock_first is part of the model specification, not a plotting choice.

The current public YAML schema does not expose adstock_first; it uses the

library default. If you need to change the composition order, use the Python

API.

Use adstock_first=True when you want the model to interpret carryover before

diminishing returns. Use False when you want each period’s spend to saturate

before the carryover step.

The code path is explicit:

True -> saturation(adstock(x))

False -> adstock(saturation(x))

Common pitfalls

Forgetting that l_max is required for adstock classes

Assuming dims automatically change transform priors even when you have

already set explicit incompatible dims on the transform

Using adstock_first=False without a substantive reason

Treating transform priors as if they were on original business units rather

than the model scale

The builder appends these effects before calling build_model(...).

Choosing between built-in and custom seasonality

Use yearly_seasonality when you need a compact built-in annual effect.

Use FourierEffect when you need:

weekly seasonality

monthly seasonality

multiple seasonal effects together

custom Fourier prefixes or priors

Common pitfalls

Adding effects after the model has already been built

Using event effect dims that do not include the required prefix

Treating yearly_seasonality and a custom yearly Fourier effect as if they

were separate concepts when they are both additive seasonal terms

Next steps

Read Time-Varying Parameters if you want trend

or media behaviour to vary smoothly over time.

Read Calibration if you want to constrain the specification

with external measurements.

Priors and Configuration

Abacus uses model_config to control priors on the underlying PyMC variables.

Transform priors can be configured either on the transform objects themselves or

through their prefixed variable names in model_config.

Abacus parses these mappings into runtime Prior or HSGPKwargs objects.

Transform priors and prefixed names

Transform parameters appear in the model under prefixed variable names.

Examples:

adstock alpha -> adstock_alpha

saturation lam -> saturation_lam

saturation beta -> saturation_beta

So you can override transform priors in either of these ways:

pass priors={...} to the transform object

override the prefixed variable in model_config

Use one style consistently within a project if you want the configuration to be

easy to read.

Directional control priors

Controls are the right place for exogenous drivers whose effect may be

negative, such as competitor spend, competitor price pressure, or supply-side

disruptions. By default, control coefficients remain unrestricted.

The current public YAML schema does not expose control_impacts or

control_sign_policy. If you need directional control settings today, use the

Python API for that part of the specification.

Constraints for directional controls

When control_impacts is configured, Abacus expects:

gamma_control and gamma_control_mundlak to be Normal or

TruncatedNormal

scalar numeric mu and sigma values for those priors

the prior dims to include "control"

If you violate those assumptions, model build fails with a validation error.

Time-varying configuration keys

When you enable a boolean time-varying effect, Abacus uses these model_config

keys:

intercept_tvp_config

media_tvp_config

Those keys can be:

an HSGPKwargs instance

a dict with HSGPKwargs fields

a dict in SoftPlusHSGP.parameterize_from_data(...) style, such as

{"ls_lower": 1, "ls_upper": 10}

dims tells PanelMMM which extra categorical axes exist alongside date.

With no extra dims, the model is indexed by:

date

channel

optionally control

With dims=("geo",), the model is indexed by:

date

geo

channel

optionally control

With dims=("geo", "brand"), it is indexed by:

date

geo

brand

channel

optionally control

What changes inside the model

Setting dims changes the coordinates and parameter shapes used in the PyMC

graph.

Quantity

No extra dims

dims=("geo",)

channel_data

("date", "channel")

("date", "geo", "channel")

target_data

("date",)

("date", "geo")

channel_contribution

("date", "channel")

("date", "geo", "channel")

control_contribution

("date", "control")

("date", "geo", "control")

intercept prior dims by default

()

("geo",)

Reserved names

Do not use these names in dims:

date

channel

control

fourier_mode

Abacus rejects them because they are reserved for internal coordinates.

dims does not imply automatic pooling

This is the most important modelling point.

By default, dims gives you parameters indexed by the panel coordinates, but

not automatic hierarchical shrinkage across those coordinates.

For example:

the default intercept prior is Normal(..., dims=dims)

transform priors default to (*dims, "channel")

control coefficients default to (*dims, "control")

Those defaults create per-slice parameters. If you want hierarchical pooling

across geo, brand, or another dimension, you need to encode that in the

priors you supply.

fit() returns an arviz.InferenceData object and also stores it on

mmm.idata.

What fit() does

When you call fit(X, y), Abacus:

checks that pandas X and y use the same index, if both are pandas

objects

builds the PyMC graph automatically if it has not been built already

merges sampler settings from the model’s sampler_config and your call-time

kwargs

runs pymc.sample(...)

computes deterministic variables and adds them to the posterior group

stores the training data in an InferenceData.fit_data group

writes model metadata into idata.attrs

That means fitted contribution variables such as channel_contribution,

intercept_contribution, and yearly_seasonality_contribution are available

in mmm.posterior after fitting when they are part of the configured model.

Configure the sampler

You can configure PyMC sampling in two places:

Where

Use it for

Precedence

sampler_config= in PanelMMM(...)

Stable defaults you want to reuse across fits

Lower

fit(..., **kwargs)

Run-specific overrides such as draws, chains, or random_seed

Higher

Abacus merges them so that explicit fit() kwargs win.

mmm=PanelMMM(date_column="date",target_column="revenue",channel_columns=["channel_1","channel_2"],adstock=GeometricAdstock(l_max=4),saturation=LogisticSaturation(),sampler_config={"draws":1000,"tune":1000,"chains":4,"target_accept":0.9,"progressbar":False,},)# Overrides draws from sampler_config, keeps target_acceptidata=mmm.fit(X,y,draws=500,random_seed=42)

Common sampler arguments

These are passed through to pymc.sample(...).

Argument

What it controls

draws

Posterior samples kept after tuning

tune

Warm-up or adaptation iterations

chains

Number of MCMC chains

cores

Number of worker processes used by PyMC

target_accept

HMC or NUTS acceptance target

progressbar

Whether PyMC shows a progress bar

random_seed

Sampling reproducibility

If you do not specify progressbar, Abacus defaults it to True unless your

sampler_config already sets it.

When to build first

For a standard workflow, call fit() directly.

Call build_model(X, y) first only when you need to inspect or modify the

graph before sampling. For example:

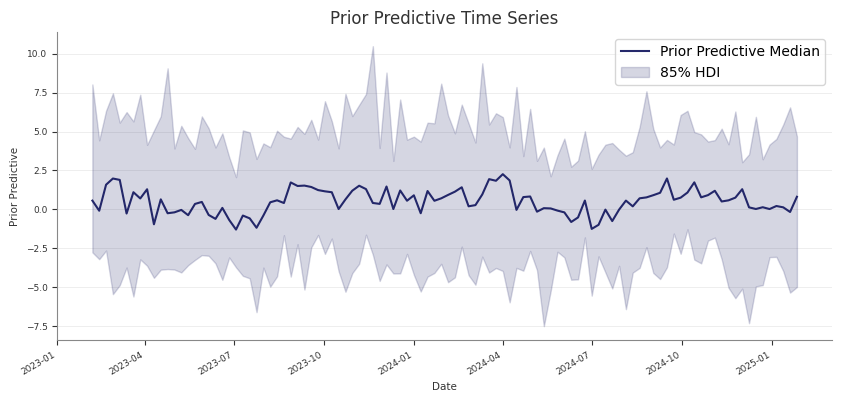

If you run prior predictive checks first and then call fit(), Abacus keeps

the existing prior and prior_predictive groups on mmm.idata.

That makes it practical to compare:

prior assumptions

posterior fit

posterior predictive behaviour

within one saved InferenceData object.

Common pitfalls

Skipping prior predictive checks and only noticing implausible priors after a

long fit

Treating prior predictive checks as a substitute for posterior predictive

assessment

Forgetting that sample_prior_predictive(...) returns extracted predictive

draws, while the full prior and prior_predictive groups are stored on

mmm.idata

Next steps

After the prior predictive behaviour looks reasonable, fit the model with

Fitting the Model.

Save and Load

Use save and load when you want to persist a fitted PanelMMM and rebuild it

later without redefining the whole model configuration in code.

save() writes the model’s InferenceData to NetCDF. load() reads that file,

recreates the PanelMMM configuration from stored metadata, restores

loaded.idata, and rebuilds the PyMC graph from the saved training data.

What Abacus stores

Abacus relies on more than the posterior draws for a full round trip.

Stored item

Why it matters

posterior and other InferenceData groups

Preserve sampled results

fit_data

Rebuild the model graph with the original training data

idata.attrs

Reconstruct PanelMMM init kwargs and validate compatibility

The stored attrs include both the shared model metadata and PanelMMM-specific

configuration such as:

date_column

channel_columns

target_column

target_type

dims

control_columns

control_impacts

adstock and saturation

adstock_first

yearly_seasonality

time_varying_intercept and time_varying_media

scaling

model_config

sampler_config

serialised mu_effects

save() behaviour

save(fname, **kwargs) is a thin wrapper over self.idata.to_netcdf(...).

Important constraints:

the model must already be fitted

self.idata must contain a posterior group

any extra kwargs are passed directly to InferenceData.to_netcdf(...)

If you call save() before fitting, Abacus raises:

RuntimeError: The model hasn't been fit yet, call .fit() first

load() and compatibility checks

By default, PanelMMM.load(...) validates that the saved file matches the

current model class and configuration:

loaded=PanelMMM.load("mmm.nc",check=True)

With check=True, Abacus verifies:

the saved model version

the saved model id derived from the serialised configuration

If those checks fail, Abacus raises DifferentModelError.

If you need to bypass those checks, you can set check=False:

loaded=PanelMMM.load("mmm.nc",check=False)

Use that only when you understand why the saved metadata does not match.

Load from an in-memory InferenceData

If you already have an InferenceData object, use load_from_idata(...)

instead of saving to disk first:

loaded=PanelMMM.load_from_idata(idata,check=True)

This is the same round-trip path that load() uses internally after reading

the NetCDF file.

Where build_from_idata() fits

build_from_idata(idata) is the lower-level rebuild step. It:

restores supported serialised mu_effects

reads idata.fit_data

splits that saved training data back into X and y

rebuilds the PyMC graph

You usually do not need to call build_from_idata() yourself because

load() and load_from_idata() already do it.

Round-trip limitations

Not every fitted object can be restored fully.

EventAdditiveEffect does not round-trip

Abacus does not deserialize EventAdditiveEffect because the original

df_events DataFrame is not stored in the saved attrs. In that case,

PanelMMM.load(...) fails fast while rebuilding the model.

Do not drop fit_data if you want to reload

Because rebuild uses idata.fit_data, do not save a partial file that omits

that group if you want to call PanelMMM.load(...) later.

But it is not a full PanelMMM round-trip artefact, because the saved file no

longer includes the training data needed for build_from_idata(...).

Practical advice

Use the default save() behaviour for round trips.

Keep check=True unless you have a specific compatibility reason not to.

Prefer PanelMMM.load(...) over loading NetCDF manually.

Refit or rebuild event effects explicitly rather than expecting saved event

state to deserialize.

Next steps

After loading a model, you can go straight to posterior predictive sampling,

diagnostics, decomposition, or optimisation using the restored idata and

rebuilt graph.

Post-Modeling

Use this section after fitting PanelMMM.

It covers posterior predictive checks, diagnostics, contribution analysis,

response curves, efficiency metrics, and the tabular summary surfaces that

Abacus exposes from fitted InferenceData.

Pages

Posterior Predictive: Sample fitted or future

predictions and compare them with observed data where available.

Diagnostics: Run design-matrix, MCMC, and predictive

diagnostics and export machine-readable reports.

Response Curves: Sample and summarise posterior

saturation and adstock curves, and understand the runner’s forward-pass

direct contribution artefacts.

ROAS and Metrics: Calculate ROAS, CPA-style metrics,

spend tables, and predictive error metrics.

Summary and Export: Work with MMMSummaryFactory,

HDI settings, time aggregation, and DataFrame export.

Subsections of Post-Modeling

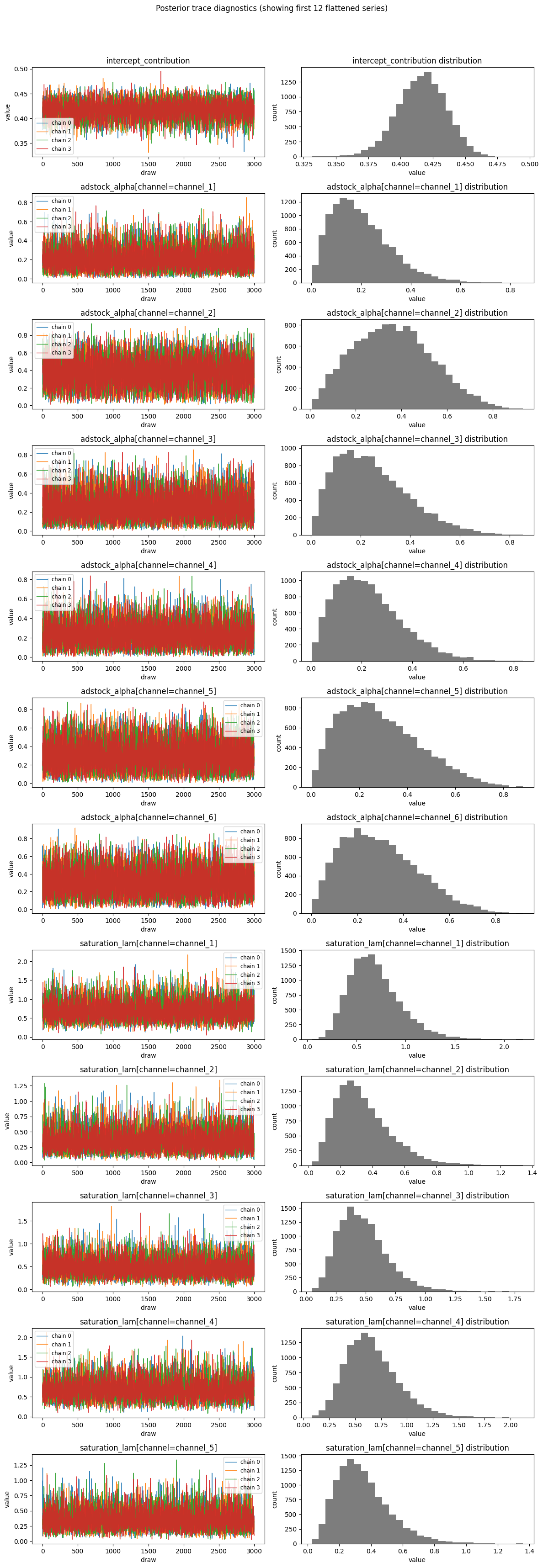

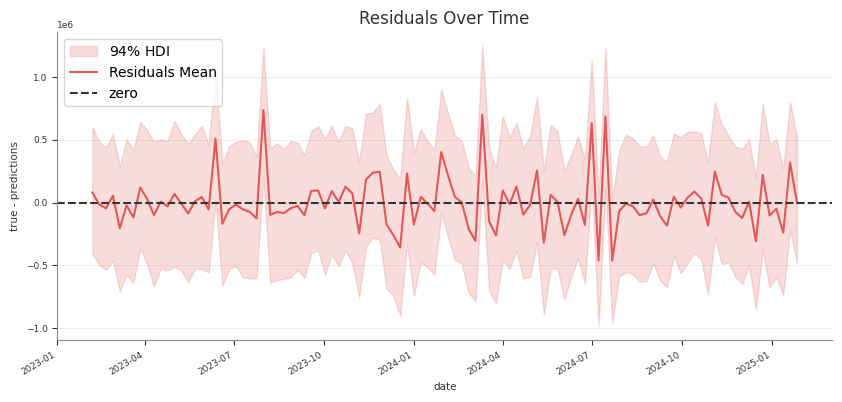

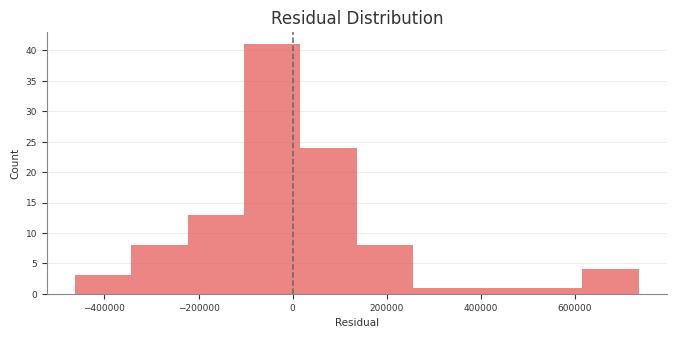

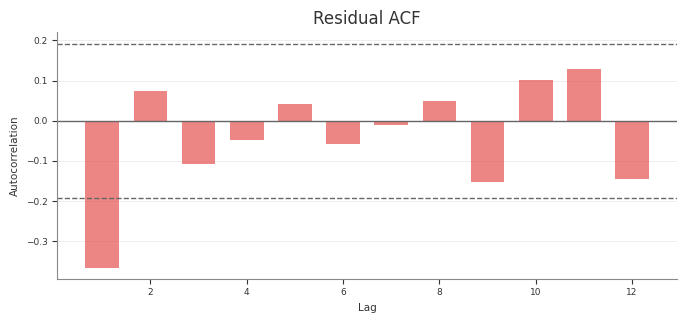

Diagnostics

Abacus exposes diagnostics through mmm.diagnostics.

Use this surface to check the design matrix, posterior sampling quality, and

posterior predictive fit. For fitted-value plots and predictive sampling, see

Posterior Predictive.

Diagnostic surfaces

mmm.diagnostics provides three groups of checks.

Area

Summary method

Report method

What it covers

Raw input screening

design_summary(X)

design_report(X)

Collinearity, constants, and near-constant regressors on raw input columns

MCMC

mcmc_summary()

mcmc_report()

r_hat, ESS, divergences, BFMI, tree depth, acceptance rate

Predictive

predictive_summary()

predictive_report()

RMSE, MAE, NRMSE, NMAE, CRPS, residual moments

The summary methods return pandas DataFrames. The report methods return typed

report objects with a to_dict() method for JSON-ready export.

Raw input screening

Use design_summary(X) on the raw design matrix you want to inspect:

design_report(X) returns a compact roll-up with matrix rank, condition

number, maximum VIF, maximum absolute correlation, and lists of flagged

variables.

Screening requirements

Raw input screening requires:

all requested columns to exist in X

all checked columns to be numeric

Abacus raises a ValueError if a variable is missing or non-numeric.

The method names stay design_summary() and design_report(), but the

pipeline now treats them as raw input screening rather than transformed model

geometry.

The same pattern works for design_report(...) and predictive_report().

Pipeline outputs

The pipeline diagnostics stage uses the same retained diagnostic surfaces to

write report tables and text summaries. If you run the pipeline, those stage

artefacts should match the behaviour documented here.

In the structured pipeline, the raw-input screening rows in

diagnostics_report.csv use the phase label raw_input_screening instead of

design so the machine-readable output matches the wording here.

Common pitfalls

Running mcmc_summary() or mcmc_report() before fitting

Running predictive diagnostics before sampling posterior predictive values

Passing non-numeric columns into design_summary(X)

Treating predictive diagnostics as a substitute for design or MCMC checks

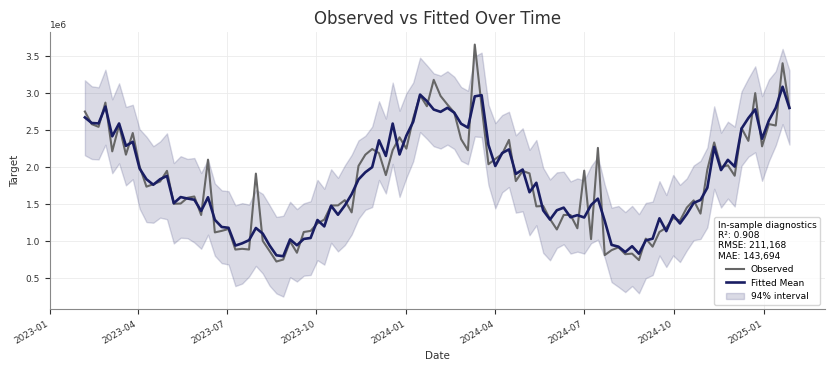

Posterior Predictive Checks

Use posterior predictive draws to check in-sample fit and to generate

predictions for new rows that follow the fitted panel layout.

If you only want the returned samples and do not want to update mmm.idata,

set extend_idata=False.

Check training-fit values against observed data

For an in-sample check, pass the same design matrix you used for fitting. This

is the same pattern used by the pipeline’s Stage 30 training-fit assessment:

sample_posterior_predictive(...) does not take y. For a holdout or future

window, keep the actual target outside the model and align it yourself if you

want external evaluation.

Use include_last_observations correctly

Set include_last_observations=True when the forecast window needs lag history

for adstock carryover.

When enabled, Abacus:

prepends the last adstock.l_max training observations internally

samples posterior predictive values on the padded data

removes the prepended rows from the returned result

This only works when the input dates do not overlap with the training dates.

If they do overlap, Abacus raises a ValueError.

Practical guidance

Use the training X for fitted-versus-observed checks.

Use future-only dates for forward prediction.

Use the training-window refit pattern for blocked holdout validation.

Keep combined=True if you want a simpler sample dimension.

Use combined=False if you need explicit chain and draw dimensions.

Call sample_posterior_predictive(...) before using

mmm.diagnostics.predictive_summary() or mmm.summary.posterior_predictive().

Common pitfalls

Calling sample_posterior_predictive(...) without X

Expecting y to be passed into the predictive method

Using include_last_observations=True on dates that overlap with training

data

Forgetting that the returned object is extracted samples, while the stored

idata.posterior_predictive group keeps the native posterior predictive

structure

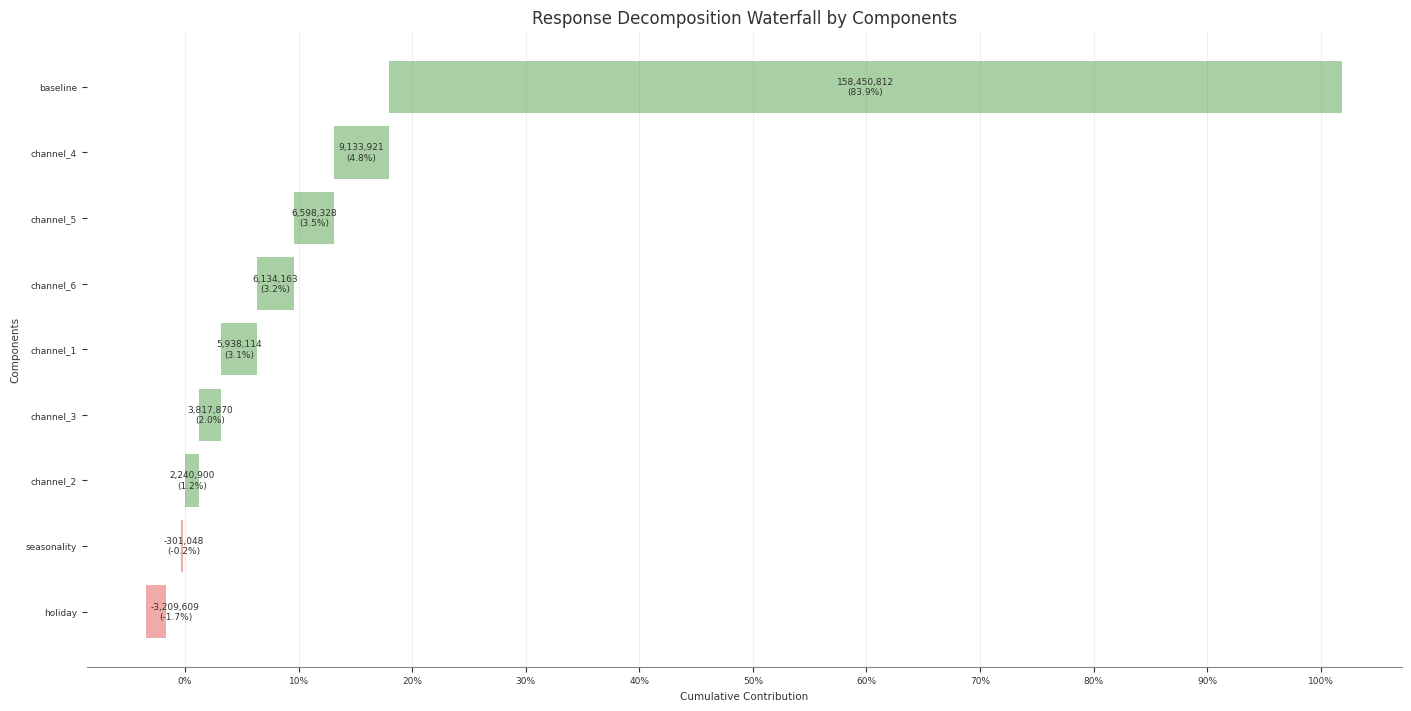

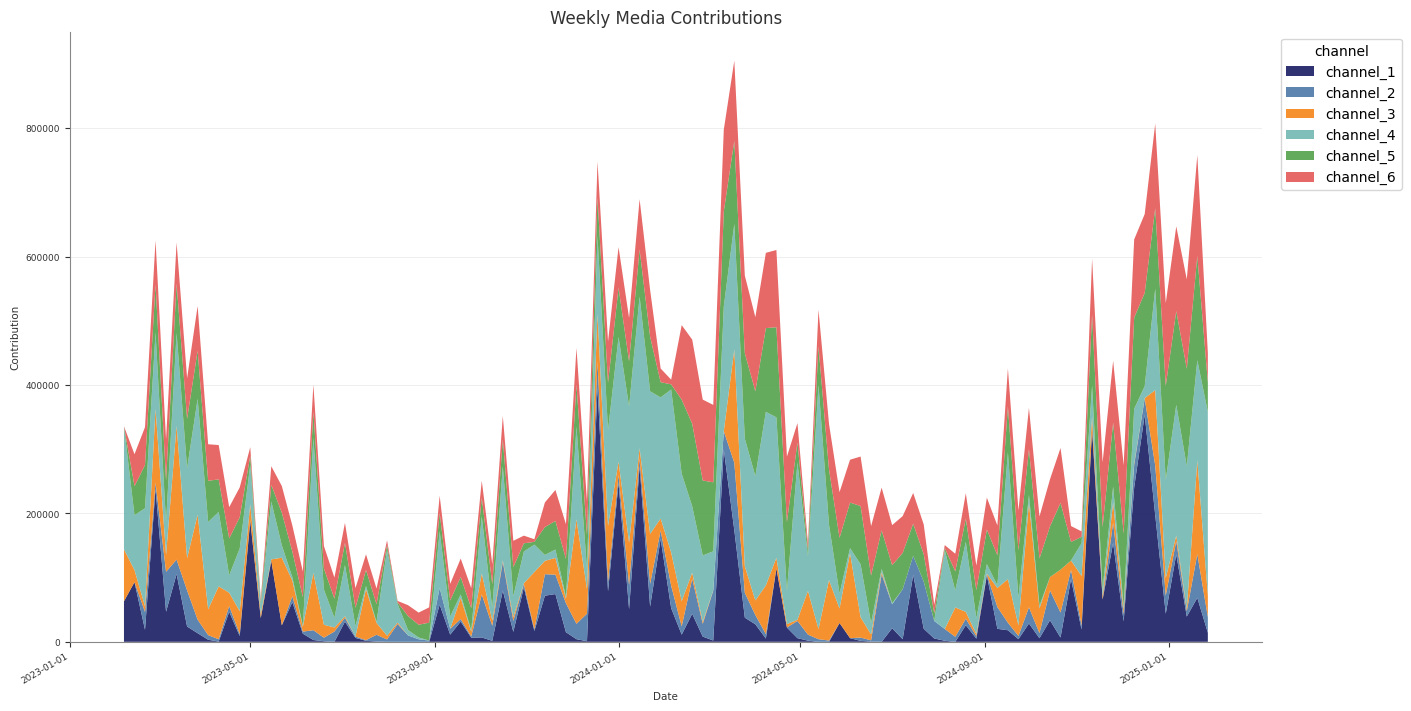

Contributions and Decomposition

Abacus stores additive contribution terms for fitted PanelMMM models and

exposes them through the data wrapper, summary tables, and plotting suite.

Use this page to inspect media, baseline, control, seasonality, and event

effects. For channel efficiency ratios built from media contributions, see

ROAS and Metrics.

Contribution surfaces

You can work with contributions at three levels.

Surface

Use it for

mmm.data

Raw xarray contribution samples

mmm.summary

DataFrames with posterior means, medians, and HDIs

mmm.plot

Time-series and waterfall visualisations

Read raw contribution samples

The lowest-level accessor is mmm.data.get_contributions(...):

identifying columns such as date, channel, control, and any panel

dims

mean

median

HDI bound columns such as abs_error_94_lower and abs_error_94_upper

mmm.summary.contributions(...) does not expose event effects. For event

effects, use mmm.data.get_contributions(include_events=True) or

mmm.summary.mean_contributions_over_time().

Create a wide decomposition table

Use mmm.summary.mean_contributions_over_time(...) when you want one row per

time point and panel slice:

Use original_scale=True when you want business-unit interpretation.

Use mmm.summary.contributions(...) for tidy per-component tables.

Use mmm.summary.mean_contributions_over_time() for decomposition exports.

Use mmm.summary.total_contribution() when you only need component-level

totals.

Common pitfalls

Expecting mmm.summary.contributions(...) to include event effects

Forgetting that baseline can include more than the intercept when Mundlak

CRE is enabled

Using frequency="all_time" with mean_contributions_over_time() or

change_over_time()

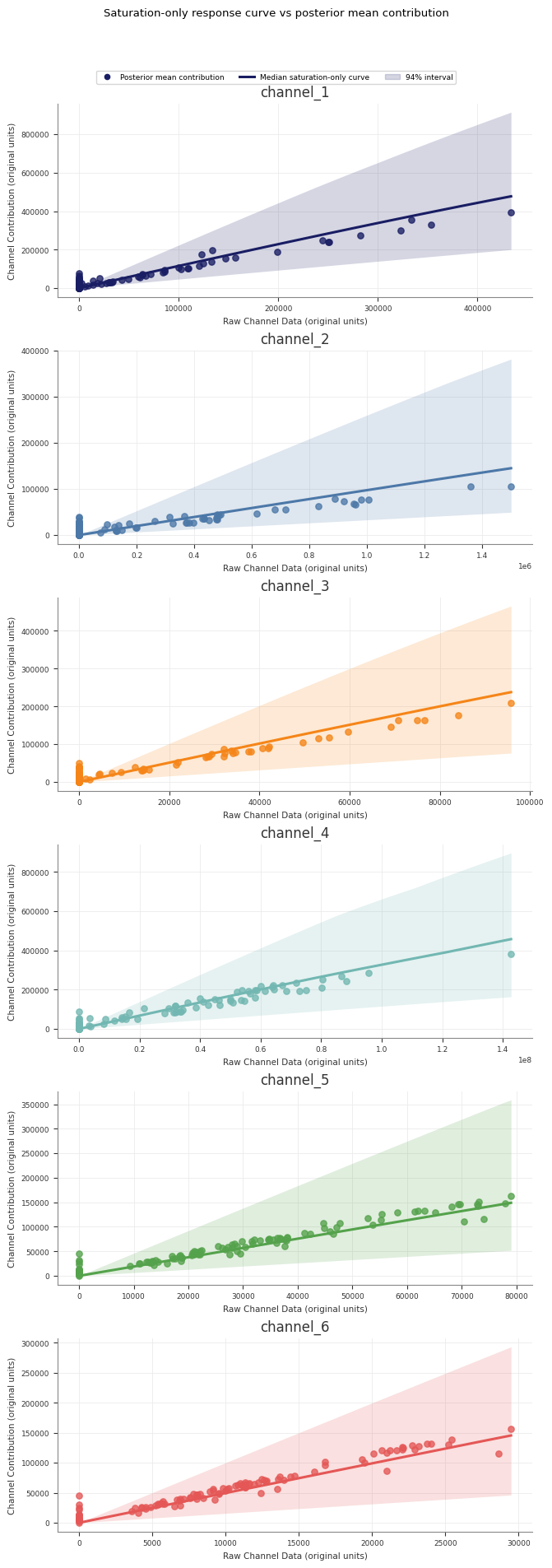

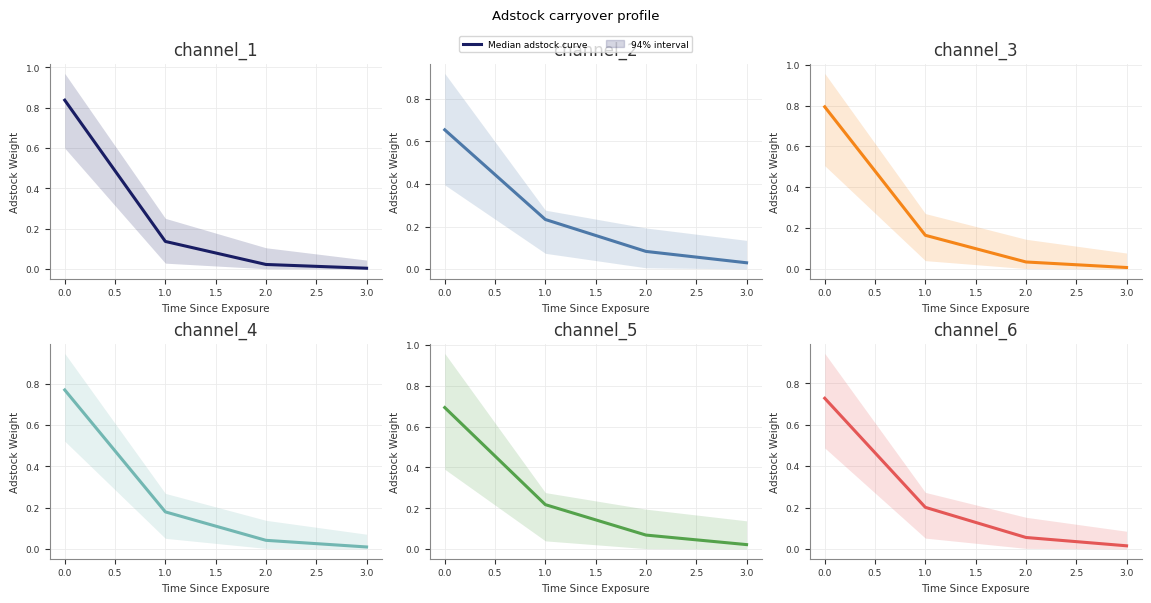

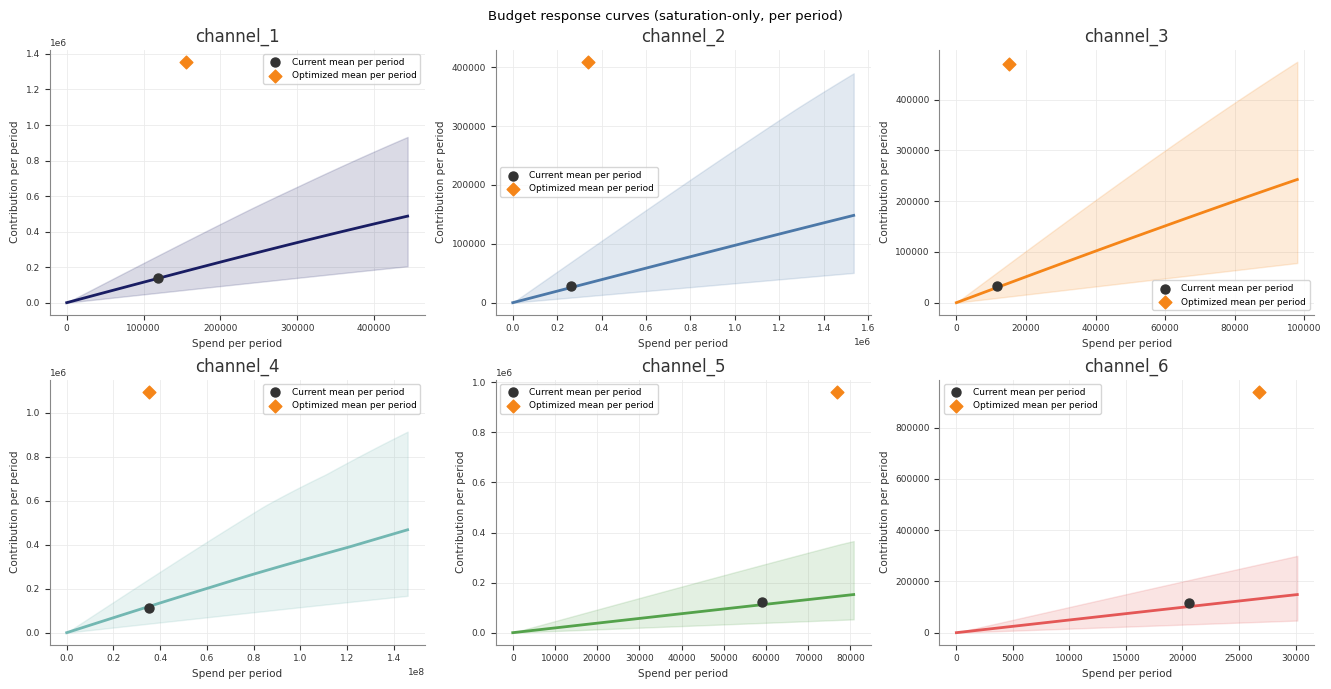

Response Curves

Use response curves to inspect the fitted media transformations directly.

Abacus exposes posterior saturation and adstock curves through both the fitted

model and mmm.summary. For decomposition of realised contributions over time,

see Contributions and Decomposition.

Sample saturation curves

Use sample_saturation_curve(...) on a fitted PanelMMM:

The adstock curve is the fitted decay pattern for an impulse of size

amount. It does not use an original_scale option because the returned

weights are not target-unit contributions.

Runner-generated direct contribution artefacts

If you use the retained pipeline runner, Stage 60_response_curves also writes

a forward-pass direct contribution artefact alongside the saturation and

adstock transformation curves:

forward_pass_contribution_curve.nc

forward_pass_contribution_curve_summary.csv

forward_pass_contribution_curve.png

This artefact is different from the saturation-only curve:

the saturation-only curve shows the fitted saturation transform itself

the forward-pass direct contribution curve runs spend through the full fitted

model path, including adstock and saturation

The retained Stage 60 forward-pass plot uses one explicit scenario so the curve

is interpretable: it rescales the full observed historical spend path from

0% to 200%, then plots total channel spend against total channel

contribution in original units. The marker at 100% highlights the fitted

total contribution for the observed historical spend path.

Expecting a dedicated file-export API on mmm.summary

Passing 94 instead of 0.94 in hdi_probs

Using saturation_curves() or adstock_curves() from a manual factory

without model=mmm

Using all_time on summaries that require a date dimension

Optimisation

This section covers Abacus budget optimisation workflows for fitted

PanelMMM models. It explains the low-level optimisation wrapper, how to

inspect optimisation outputs.

For the higher-level planner service and Dash UI, see

Scenario Planning.

Pages

Budget Optimisation - How to run

PanelBudgetOptimizerWrapper, set bounds and masks, and define spend over a

future window.

Interpreting Optimisation - How to read the

allocation output, inspect simulated response samples, and use the pipeline

optimisation artefacts.

Scenario Planning - How to compare current, manual,

and fixed-budget optimised scenarios with the planner service and optional

Dash UI.

Subsections of Optimisation

Budget Optimisation

Use PanelBudgetOptimizerWrapper when you want to optimise spend for a fitted

PanelMMM over a future date window.

The wrapper builds a synthetic future dataset for the requested window, swaps

the model’s channel_data for an optimisation variable, and then calls the

generic BudgetOptimizer. If you want to compare several plans in total

horizon spend units, see Scenario Planning.

What the optimiser maximises

For PanelBudgetOptimizerWrapper, optimize_budget() defaults to:

The optimiser therefore maximises the average posterior response of the chosen

response variable, subject to your budget bounds and constraints.

Budget units

The low-level wrapper uses per-period spend units.

budget is the total spend across all optimised cells for one model period.

The returned allocation has no date dimension, so Abacus repeats that

allocation across the optimisation window.

If the window has num_periods=8 and you pass budget=100_000, the

simulated spend over the full horizon is 800_000 before any carryover

effects are applied.

This is different from Scenario Planning, which

treats total_budget and manual allocations as total horizon spend and

converts them to per-period units internally.

The Stage 70 pipeline optimisation uses the same units as the low-level

wrapper because it passes optimization.total_budget directly to

PanelBudgetOptimizerWrapper.optimize_budget(...).

Required inputs

Input

What Abacus expects

Notes

model

A fitted PanelMMM with idata.posterior

The optimiser needs posterior draws and model graph variables.

start_date, end_date

A future window at the model’s observed date frequency

Abacus infers num_periods from the training data frequency.

allocation is an xarray.DataArray over the non-date budget dimensions.

For a model with dims=("geo",), the result dims are typically

("geo", "channel").

Bounds and masks

budget_bounds

Use budget_bounds to cap spend for each optimised cell.

If the budget has only one non-date dimension, you can pass a dict such as

{"tv": (0.0, 50_000.0), "search": (0.0, 30_000.0)}.

For panel budgets, pass an xarray.DataArray with dims

(*budget_dims, "bound"), where "bound" contains "lower" and "upper".

If you omit budget_bounds, Abacus warns and uses (0, total_budget) for

every optimised cell.

Abacus reindexes DataArray bounds to the model’s internal coordinate order,

so the input coordinate order does not need to match exactly.

budgets_to_optimize

Use budgets_to_optimize to choose which cells can move.

The mask must be a boolean xarray.DataArray over the budget dimensions.

Unoptimised cells are fixed at zero in the returned allocation.

If you omit the mask, Abacus optimises every cell where the fitted model has

non-zero historical channel_contribution information.

If your mask includes True for a cell where the model has no information,

Abacus raises ValueError.

Time distribution across the window

Use budget_distribution_over_period to flight each allocation cell over time

instead of repeating the same spend every period.

The object must be an xarray.DataArray with:

dims exactly ("date", *budget_dims)

one date weight per optimisation period

weights that sum to 1 across the date dimension for every budget cell

Use the same budget_distribution_over_period again when you call

sample_response_distribution(),

otherwise you will optimise one spend path and simulate another.

For response simulation through the wrapper, the date coordinates can be:

integer positions 0 .. num_periods - 1, or

exact dates that match the optimisation window

Constraints and solver controls

default_constraints=True adds the default equality constraint:

sum(allocation) == budget

This is enabled by default and emits a warning so you can see that the default

constraint set is active.

You can also pass:

extra SciPy minimise keyword arguments directly to optimize_budget(...) to

tweak the underlying solver call

callback=True to get a third return value with per-iteration objective,

gradient, and constraint diagnostics

YAML note for the pipeline runner

If you run optimisation through the structured pipeline, configure the

optimization block in YAML:

In this pipeline path, optimization.total_budget uses the wrapper contract

described above: it is passed straight to optimize_budget(...) as

per-period spend, not total horizon spend.

Common pitfalls

Passing a total horizon budget to optimize_budget(...). Divide by

wrapper.num_periods first, or use Scenario Planning.

Passing dict bounds for a panel budget. Dict bounds only work when the budget

dims are just ("channel",).

Omitting a budget dimension from budget_distribution_over_period. The

distribution must include every budget dim, not just the one you want to vary.

Forgetting that response_variable must exist in the fitted optimisation

graph.

Using one budget distribution for optimisation and a different one for

response simulation.

allocation is an xarray.DataArray over the non-date budget dimensions.

Model shape

Typical allocation dims

Meaning

No extra panel dims

("channel",)

One optimised value per channel

dims=("geo",)

("geo", "channel")

One value per (geo, channel) cell

dims=("geo", "brand")

("geo", "brand", "channel")

One value per (geo, brand, channel) cell

The values are in the wrapper’s per-period units. Unoptimised cells are

present and set to zero.

result

result is SciPy’s OptimizeResult. The fields you will usually inspect are:

Field

Meaning

success

Whether the solver converged

status

SciPy status code

message

Human-readable solver message

fun

Final objective value

nit

Number of iterations

x

The optimised flat parameter vector

If success is False, Abacus raises MinimizeException unless you opt in to

return_if_fail=True on the underlying BudgetOptimizer.

callback_info

When callback=True, Abacus records one entry per solver iteration. Each entry

includes:

x

fun

jac

constraint_info when constraints are active

Use this when you need to diagnose solver behaviour rather than just consume the

final allocation.

Simulate the optimised plan

The optimiser itself returns only the allocation. To estimate spend paths and

contributions over the requested window, call sample_response_distribution().

Set noise_level=0.0 when you want the spend path to match the requested

allocation exactly.

What response_samples contains

The wrapper builds a synthetic future dataset, samples posterior predictive

draws, and then merges the requested allocation and simulated spend path back

into the result.

response_samples therefore contains:

Variable

Source

Meaning

allocation

Added by the wrapper

Requested allocation without a date dimension

One variable per channel

Added by the wrapper

Simulated spend path over the future dates

mmm.output_var

Posterior predictive sample

Model output variable

channel_contribution

Posterior predictive sample

Channel contribution on model scale

total_media_contribution_original_scale

Posterior predictive sample

Total media contribution on the original target scale

If you pass additional_var_names, Abacus also includes those variables when

they exist in the model graph.

Carryover and evaluation window

include_carryover=True changes how Abacus builds the synthetic future window.

Abacus extends the generated dates by adstock.l_max periods.

It then zeroes the tail spend rows after the requested window.

The extra dates let posterior predictive sampling include lagged effects from

the planned spend.

This is why the simulated dataset can cover a longer evaluated window than the

requested start_date to end_date range, while still preserving the same

total spend.

Plot the result

The plotting helpers under mmm.plot are designed to work directly with the

response dataset returned by the wrapper.

split_by="geo" or another dimension to create separate subplots

original_scale=True to prefer original-scale contribution variables when

they are available

Example optimisation output:

Read the Stage 70 pipeline artefacts

If you run optimisation through python -m abacus.pipeline.runner, Stage 70

writes both the low-level optimiser output and several interpretation files.

Use this section when you want to compare historical, manual, and optimised

future plans with abacus.scenario_planner.

The scenario planner is a higher-level planning surface than the low-level

optimisation wrapper. It works in total horizon spend units, returns structured

comparison tables, and includes a supported workspace app for fitted runs.

Pages

Supported Surface: The recommended planner entry

points, fitted-run contract, persisted workspace state, and beta limits.

Overview and Workflow: What the planner does,

how it differs from low-level optimisation, and how scenario windows work.

Scenario Specifications: The public scenario

spec classes, allocation shapes, bounds, and budget distributions.

Python API: How to use ScenarioPlanner.evaluate(...) and

the supported workspace helpers from Python.

Comparison Outputs: The structure and meaning of

ScenarioResult, ScenarioComparison, and the output tables.

Dash App: How to launch the supported workspace UI from a

fitted run, work with saved workspaces, and understand background jobs.

Subsections of Scenario Planning

Overview and Workflow

Use the scenario planner when you want to compare whole plans rather than run a

single low-level optimisation call.

The planner combines three things:

typed scenario specifications

a Python comparison service

a supported workspace app for fitted results directories

For the supported beta entry points and current limits, see

Supported Surface.

What the planner compares

The retained planner supports three scenario types:

Scenario type

Purpose

Public spec

Current

Use observed history as a reference plan

CurrentScenarioSpec

Manual allocation

Simulate a user-defined future plan

ManualAllocationScenarioSpec

Fixed-budget optimised

Optimise a future plan at a fixed budget

FixedBudgetOptimizedScenarioSpec

Planner units versus optimiser units

The most important distinction is budget units.

Surface

Public budget contract

PanelBudgetOptimizerWrapper

Per-period spend

ScenarioPlanner

Total spend over the whole scenario horizon

For example, if a four-period scenario has a total budget of 900_000, the

planner converts that to per-period units internally before it calls the

wrapper or response sampler.

Requested and evaluated windows

Each scenario has a requested window from start_date to end_date.

For simulated scenarios, the evaluated window can be longer than the requested

window when you set include_carryover=True. Abacus extends the synthetic

future path so lagged adstock effects can continue after the requested end

date.

The planner reports both windows in the metadata output.

Historical overlap for current scenarios

CurrentScenarioSpec is strict about history.

Its requested window must overlap observed data. Abacus does not reinterpret a

future-only window as “use the latest history instead”.

Typical workflow

The common workflow is:

Fit PanelMMM.

Build one or more scenario specs.

Either run ScenarioPlanner.compare(...) or launch the workspace app from

the fitted run directory.

Inspect the comparison tables, save workspaces, and export the planning

outputs you need.

Mixing up total horizon spend and per-period spend

Using a future-only window in CurrentScenarioSpec

Forgetting that carryover can extend the evaluated window

Scenario Specifications

This page documents the public spec classes under abacus.scenario_planner.

Most users create one of the three concrete scenario specs:

CurrentScenarioSpec

ManualAllocationScenarioSpec

FixedBudgetOptimizedScenarioSpec

Abacus also exposes shared base models such as

HistoricalReferenceScenarioSpec and SimulatedScenarioSpec, but you do not

normally instantiate those directly.

Shared fields

All public scenario specs inherit these core fields:

Field

Meaning

name

Display name for the scenario

start_date

Requested scenario start date

end_date

Requested scenario end date

scenario_id

Stable scenario key used in outputs

If you do not set scenario_id, Abacus derives one by slugifying name.

Scenario IDs must be unique within one ScenarioPlanner.compare(...) call.

CurrentScenarioSpec

Use CurrentScenarioSpec for a historical reference plan.

ScenarioComparison is a row-wise concatenation of the individual scenario

results, with scenario identifiers added to every table.

totals

totals has one row per scenario.

It includes:

scenario_id

scenario_name

scenario_type

total_spend

contribution_mean

contribution_median

contribution_hdi_94_lower

contribution_hdi_94_upper

efficiency_metric

efficiency_mean

efficiency_median

efficiency_hdi_94_lower

efficiency_hdi_94_upper

efficiency_metric is ROAS for revenue targets and CPA for conversion

targets.

channels

channels has one row per (scenario, channel).

It includes:

scenario identifiers

channel

spend

spend_share

spend_per_period

contribution summary columns

contribution-per-period columns

efficiency summary columns

efficiency_metric

The planner aggregates non-channel panel dims before it builds this table. For

example, a (geo, channel) model still returns one row per channel here.

contributions_over_time

contributions_over_time has one row per (scenario, date, channel).

It includes:

scenario identifiers

date

channel

contribution_mean

contribution_median

contribution_hdi_94_lower

contribution_hdi_94_upper

Like channels, this table aggregates non-channel panel dims before

summarising.

allocations

allocations keeps the original allocation grain.

It includes:

scenario identifiers

the allocation dims, such as channel, geo, or brand

allocation

realized_spend

For current scenarios, allocation is the summed historical spend over the

reference window. For simulated scenarios, allocation is the requested total

horizon allocation and realized_spend is the realised spend from the response

simulation.

metadata

metadata is the audit table for each scenario.

Shared fields include:

scenario_id

scenario_name

scenario_type

start_date

end_date

evaluated_start_date

evaluated_end_date

num_periods

target_type

efficiency_metric

Additional fields depend on scenario type.

Current scenario metadata

Current scenarios add:

reference_window_dates

Manual scenario metadata

Manual scenarios add:

requested_total_budget

total_budget

reference_window_dates

budget_unit

Fixed-budget optimised metadata

Optimised scenarios add:

requested_total_budget

total_budget

optimization_success

optimization_status

optimization_message

optimization_objective_value

reference_window_dates

budget_unit

Requested versus evaluated windows

The metadata table is the best place to check whether the evaluated window

matches the requested window.

When include_carryover=True, the evaluated end date can be later than the

requested end_date.

ScenarioComparison.to_store_payload() converts the comparison tables into a

JSON-friendly dict of record lists:

payload=comparison.to_store_payload()

This is the payload format consumed by the supported workspace app.

Common pitfalls

Reading channels as if it retained non-channel panel dims

Ignoring metadata when carryover is enabled

Comparing requested allocation with realised spend without checking the

allocations table

Supported Surface

Use this page to understand which Scenario Planner entry points Abacus

supports for beta evaluation.

The planner has two primary surfaces:

a Python comparison API for scripted planning workflows

a workspace-based Dash app for interactive scenario editing and review

Recommended entry points

Use these entry points in preference order.

Entry point

Use it when you want to

Notes

ScenarioPlanner

evaluate or compare scenarios from Python

Best fit for notebooks, scripts, and testable planning flows

python -m abacus.scenario_planner

launch the supported interactive app from a fitted run directory

Starts the workspace UI with file-backed persistence

create_app_from_results_dir(...)

embed the supported app in your own Python launcher

Returns app, run_context, workspace_service, and workspace

load_workspace_bundle(...)

load the fitted run and active workspace without starting Dash

Useful for custom wrappers around the supported app

WorkspaceService

work with saved workspaces programmatically

Advanced surface for cloning, saving, evaluating, sweeping, and exporting

Advanced integration surfaces

Abacus also exposes lower-level objects such as:

create_scenario_planner_dash_app(...)

ThreadedScenarioPlannerJobRunner

SynchronousScenarioPlannerJobRunner

WorkspaceStore

These are public, but they are more implementation-shaped than the recommended

entry points above. Use them when you need to embed the planner into a custom

application or override the default job runner or storage behaviour.

Results directory contract

The supported launcher and load_workspace_bundle(...) expect a fitted run

directory, not raw modelling inputs.

The run directory must include:

Requirement

Why it matters

run_manifest.json

Abacus uses it to locate the config and saved artefacts

a fit-stage idata artefact

Abacus attaches the saved posterior to the rebuilt model

When metadata-stage config artifacts are present, Abacus prefers those

in-run files when rebuilding the saved PanelMMM:

00_run_metadata/config.resolved.yaml

00_run_metadata/config.original.yaml

the copied config file under 00_run_metadata/

Only when those in-run config artifacts are absent does the planner fall back

to run_manifest.json["config_path"].

That makes the supported loader more portable when the original config path is

no longer available, but it does not guarantee full relocation across

machines. The chosen config can still reference dataset files outside the run

directory.

The planner can also load these optional optimisation artefacts when they are

present:

70_optimisation/budget_response_curves.csv

70_optimisation/budget_bounds_audit.csv

When these files are available, the app can show saved saturation-reference

response-curve and bounds-audit views.

What the app persists

The workspace app stores its own planning state under the fitted run

directory:

Abacus includes a supported Dash app for workspace-based scenario planning.

Use it when you already have a fitted run directory and want to inspect,

edit, evaluate, compare, sweep, and export scenarios without writing the

entire workflow by hand.

The app does not fit PanelMMM. It loads an existing fitted run, reuses the

saved idata, and evaluates planner scenarios against that fitted model.

For the recommended entry points and beta scope, see

Supported Surface.

Install the optional dependencies

python -m pip install -e ".[planner]"

The planner extra installs the Dash and Plotly dependencies used by the UI.

Launch the supported app

Use the supported module launcher for fitted pipeline results:

This launcher is the recommended interactive entry point for beta evaluation.

It loads the fitted run, opens or seeds a planner workspace, and starts the

app with the threaded job runner used by the supported UI.

Useful flags:

--workspace-id to open one previously saved workspace

--workspace-name to control the seeded workspace name

--current-periods and --future-periods to change the default seeded windows

--budget-scale to scale the default future budget

--build-only to validate the run and print a summary without starting Dash

Abacus also still exposes the lower-level

create_scenario_planner_dash_app(...) factory when you already have a

ScenarioComparison or ScenarioWorkspace.

What the launcher requires

The supported launcher expects a fitted results directory that contains:

run_manifest.json

a fit-stage idata artefact

When the metadata stage is present, the launcher prefers the in-run config

artifacts under 00_run_metadata/ and only falls back to

run_manifest.json["config_path"] if those files are absent.

In build-only mode, the launcher prints the selected config path and its

provenance so you can see whether the planner loaded:

resolved_in_run

original_in_run

copied_in_run

external_manifest_path

This makes the launcher more portable when the original config path no longer

exists, but the chosen config can still fail if it references dataset files

that are not present on the current machine.

When these optional files are present, the app also loads them for richer UI

views:

70_optimisation/budget_response_curves.csv

70_optimisation/budget_bounds_audit.csv

What the UI includes

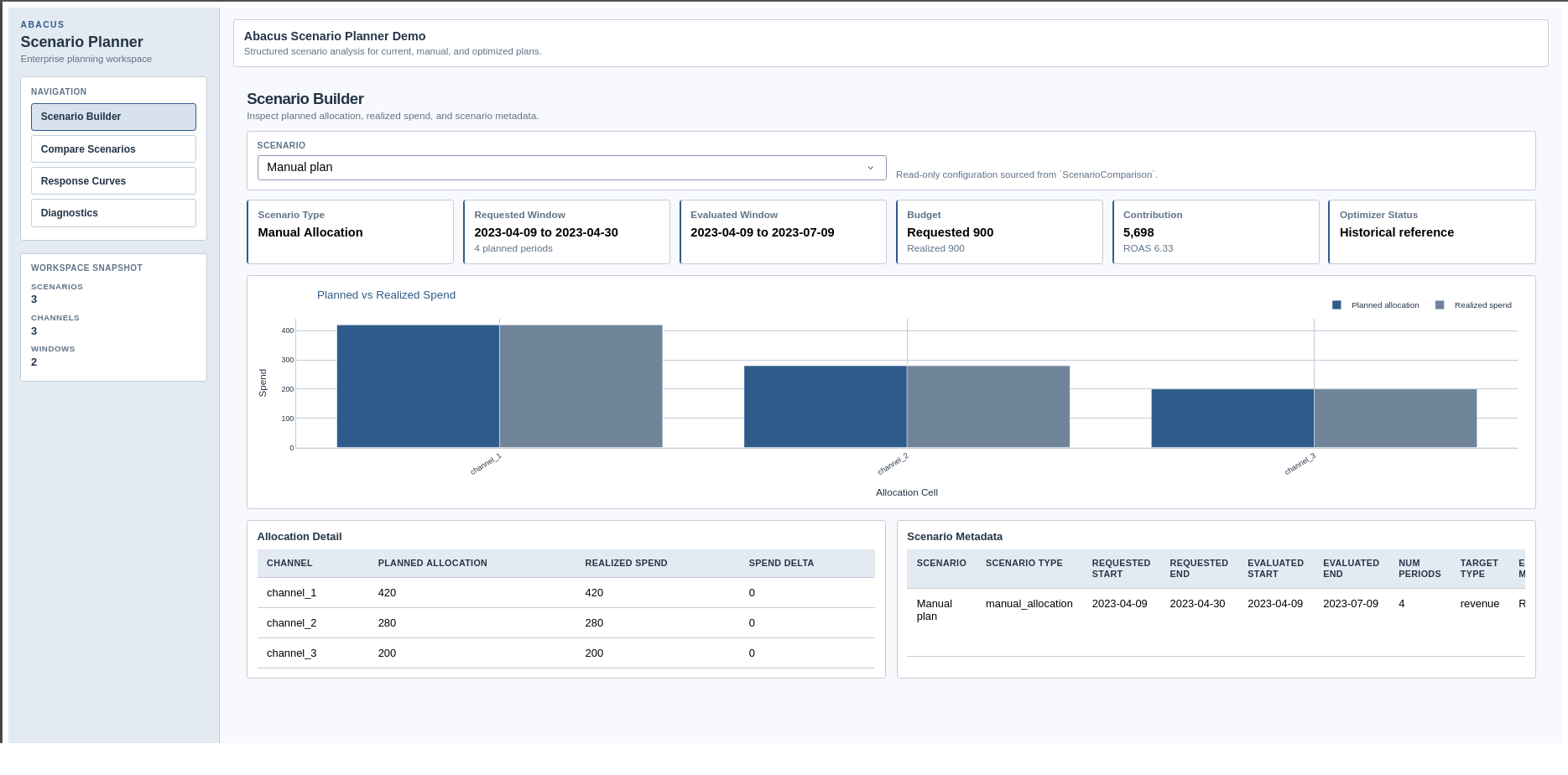

The current app has five tabs:

Plan Setup for run context, workspace metadata, saved workspaces, draft inventory, and the launch path into Scenario Builder

Scenario Builder for editing one draft at a time and evaluating it back into the workspace

Review for cross-scenario totals, deltas, rankings, movers, and approval/export readiness

Explain for response curves, operating-region views, lift comparisons, and diagnostics/audit surfaces

Export for reproducible export bundles and deterministic sensitivity output selection

What the app saves

The workspace app persists planning state under the fitted run directory:

Path

What Abacus saves

scenario_planner/workspaces/

workspace JSON files and compact manifests

scenario_planner/cache/

cached evaluated scenarios and cache index

scenario_planner/exports/

export bundles and zipped archives

This means a planner session stays attached to one fitted run.

Plan Setup page

The Plan Setup page shows the loaded run context and the active planner

workspace. It also lets you:

open a different saved workspace for the same run

clone the current workspace into a new planning branch

edit workspace name, owner, tags, and notes

inspect revision history, job history, and evaluation-cache reuse

launch the current workspace into Scenario Builder

This page is the planner launch surface: planning context stays visible first,

while operational details remain available through collapsed secondary

sections.

Scenario Builder page

The Scenario Builder page is interactive. You can:

create current, manual_allocation, and fixed_budget_optimized drafts

duplicate or delete drafts

edit names, dates, carryover, budget, and manual allocations

capture scenario owner, workflow status, approvals, pinning, tags, and notes

evaluate and save the draft back into the workspace

When a draft has been evaluated, the page shows planned versus realised spend,

allocation detail, and scenario metadata. When a draft has changed but has not

yet been re-evaluated, the page shows a draft preview instead.

Scenario Builder page in the supported Dash app.

Review page

The Review page focuses on scenario-to-scenario trade-offs and review

readiness. It includes:

scenario summary cards

overview and delta charts

channel comparison charts

scenario ranking and top-mover tables

contribution-over-time comparisons

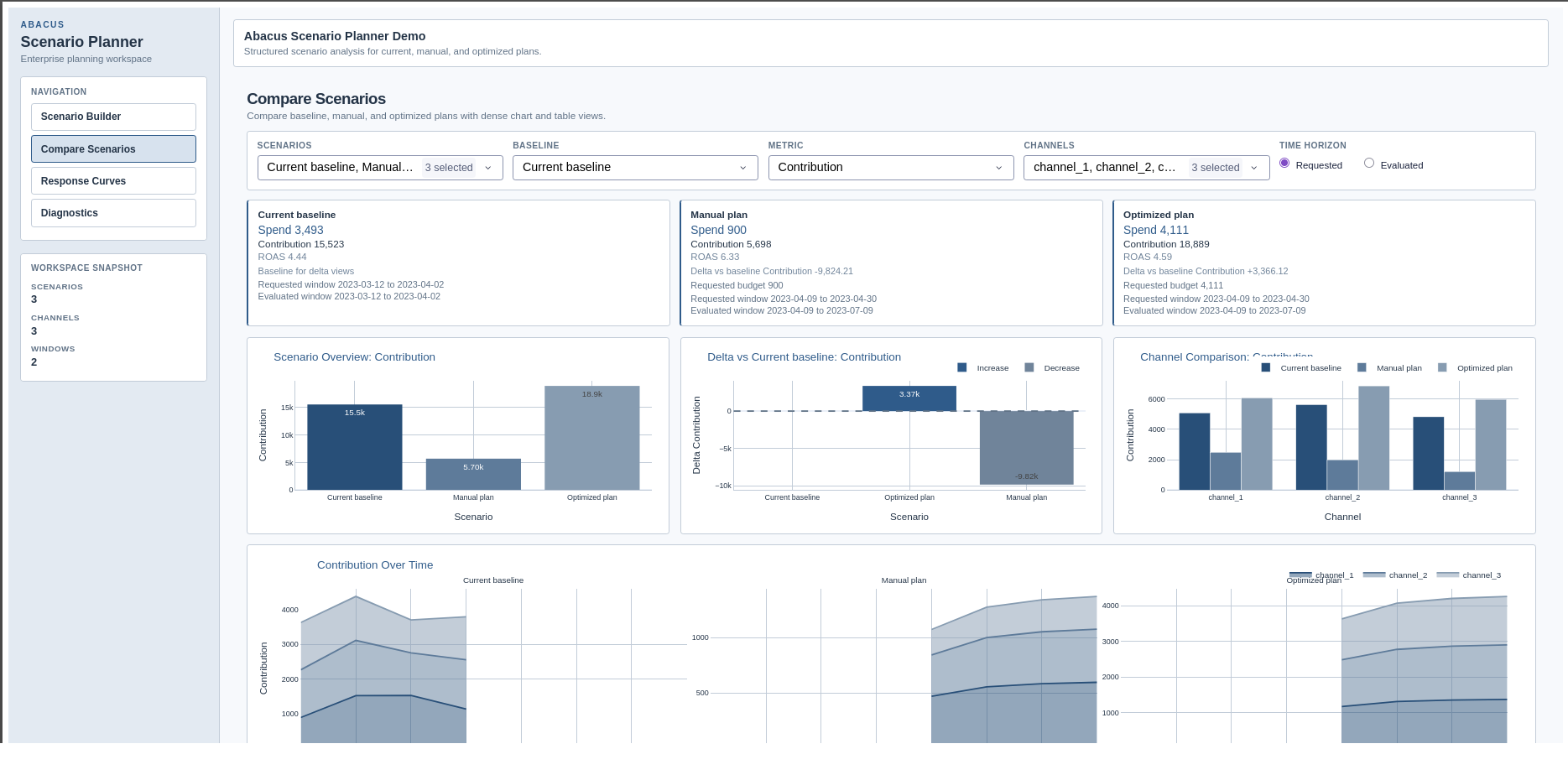

Compare Scenarios page in the supported Dash app.

Explain and Export pages

The remaining tabs build on the same workspace state:

Explain overlays scenario reference points on the saved Stage 70 saturation-only response-curve artefact when available

the plotted marker position follows the saved reference curve at each scenario’s spend-per-period level

marker hover text also shows the actual evaluated average contribution so you can compare the scenario outcome with the reference-curve position

Explain also surfaces scenario warnings, optimiser status, bounds audit, allocation reconciliation, operating-region views, and lift comparisons

Export writes reproducible bundles under the run directory and exposes any saved sensitivity output selections

Background jobs

The supported app runs draft evaluation and sensitivity sweeps as background

jobs.

In the current beta:

the app queues draft evaluation and sensitivity sweeps

the UI polls the active job and refreshes the workspace when the job completes

export runs synchronously, but Abacus still records it in job history

The UI currently tracks one active planner job at a time. Finish the current

evaluation or sweep before starting another one.

Practical guidance

Launch the app from a fitted results directory, not from raw input data.

Use separate cloned workspaces for competing planning narratives.

Re-evaluate a draft after changing dates, budget, or allocation values.

Check both requested and evaluated windows when carryover is enabled.

Review the Diagnostics page before exporting or sharing a scenario set.

Treat the built-in launcher as a local beta workflow rather than a production deployment surface.

Common pitfalls

Launching the app without installing .[planner]

Pointing the launcher at a directory without run_manifest.json and fit artefacts

Expecting the app to fit a model from scratch

Interpreting a draft preview as evaluated output before clicking Evaluate and Save

Starting a second evaluation or sweep while another planner job is still running

Pipeline Runner

This section covers the structured abacus.pipeline runner: how it loads a

config and dataset, executes the retained stage sequence, and writes

reproducible run artefacts to disk.

Pages

Runner Overview - How run_pipeline(...) works, which

stages run, and when the optimisation stage is skipped.

YAML Configuration - Which YAML keys the runner

consumes and how they map to model build, data loading, holidays, and

optimisation.

CLI Reference - The thin python -m abacus.pipeline.runner

interface and its supported flags.

Output Directory Schema - The run directory

layout, manifest schema, stage statuses, and main artefacts.

Extending the Runner - How to add a stage or wire

in reporting without bypassing the manifest and artifact helpers.

Subsections of Pipeline Runner

Runner Overview

Use the pipeline runner when you want a full disk-backed PanelMMM run instead

of only an in-memory fit.

The runner loads a YAML config and a CSV dataset, builds the model, executes a

fixed stage sequence, and writes each stage’s artefacts into a structured run

directory. When validation is enabled, the runner performs a second train-window

fit for the blocked holdout stage, so the run takes longer than a pure

full-sample fit.

The path to run_manifest.json inside that directory

What the runner does

run_pipeline(...) performs these steps:

Load the YAML config with load_yaml_config(...).

Load X and y from CSV using load_pipeline_data(...).

Merge CLI sampler overrides with YAML fit through

build_model_kwargs(...).

Create the output directory tree and initialise run_manifest.json.

Run the retained stages in order, updating the manifest after every stage.

The model is built in Stage 00 by build_mmm_from_yaml(...), then stored in the

shared PipelineContext for the remaining stages. Runner-only roots such as

diagnostics and validation stay on the pipeline context and are stripped

before the public MMM builder validates the model YAML.

Stage order

The runner uses a fixed stage list.

Stage key

Directory

Purpose

Optional

metadata

00_run_metadata

Build the model and write resolved config and dataset metadata

No

preflight

10_pre_diagnostics

Prior predictive draws and plot

No

fit

20_model_fit

Fit the model, save InferenceData, write trace and summary

Raw input screening, MCMC, predictive, and residual diagnostics

No

curves

60_response_curves

Saturation-only, forward-pass direct contribution, and adstock curve artefacts

No

optimisation

70_optimisation

Budget optimisation artefacts

Yes

The validation stage is marked skipped when the YAML config does not contain

validation or it is disabled. The optimisation stage is also optional; it

returns None and is marked skipped when the YAML config does not contain an

optimization block.

PipelineRunConfig controls runtime settings that sit outside the YAML model

specification.

Field

Purpose

config_path

YAML file to load

output_dir

Root directory under which the run directory is created

run_name

Optional run-name override; otherwise the config filename stem

dataset_path

Optional combined dataset CSV override

x_path, y_path

Optional feature and target CSV overrides

holidays_path

Optional holiday CSV override

target_column

Target column name used during CSV loading

prior_samples

Number of prior predictive samples for Stage 10

draws, tune, chains, cores, random_seed

Sampler overrides merged onto YAML fit

curve_samples, curve_points

Curve sampling settings for Stage 60

Only sampler settings are merged into model construction. Other overrides are

used by the runner itself during data loading, holiday resolution, diagnostics

reporting, and output setup.

The pipeline runner reads the same YAML model specification used by

build_mmm_from_yaml(...), then adds a small set of runner-specific conventions

for data loading, optional blocked holdout validation, and Stage 70

optimisation.

This page documents the keys that the runner actually consumes.

Root keys

Key

Required

Used for

data

Usually

Resolve dataset paths when you do not pass dataset_path, x_path, or y_path through PipelineRunConfig

target

Yes

Define the target column and business target type

dimensions

No

Declare panel-dimension columns such as geo or brand

media

Yes

Define channel/control columns and transform types

scaling

No

Configure target/channel scaling rules

effects

No

Append additive effects in YAML order before build_model(...)

priors

No

Override model-level priors and prefixed transform priors

fit

No

Default sampler settings for Stage 20 fitting

holidays

No

Add holiday events before model build

original_scale_vars

No

Add original-scale contribution variables before fitting

inference_data

No

Attach existing InferenceData when the file exists

The builder appends each effect to model.mu_effects in YAML order before

calling build_model(...).

holidays

The holidays block is optional.

Supported keys used by the builder include:

Key

Meaning

path

Holiday CSV path

enabled

Set to false to disable holiday loading

prefix

Prefix for generated holiday effect coordinates

countries

Optional country filter for catalogue-style holiday CSV input

Example:

holidays:path:"holidays.csv"prefix:"holiday"

The CLI or PipelineRunConfig.holidays_path overrides holidays.path.

If you omit both path and the override but still configure holidays,

Abacus falls back to the bundled abacus.data:holidays.csv.

original_scale_vars

Use original_scale_vars when you want specific contribution variables to be

available on the original target scale:

original_scale_vars:- channel_contribution- y

The builder applies these through

model.add_original_scale_contribution_variable(...) before fitting.

inference_data

inference_data.path is passed through to the YAML builder. If the file exists, Abacus

attaches that InferenceData to the built model during Stage 00.

Important: the structured runner still executes Stage 20 and fits the model

again. inference_data.path does not currently skip fitting.

optimization

Add an optimization block when you want Stage 70 to run. If this block is

absent, Stage 70 is marked skipped.

The YAML builder validates this block when the config is loaded. The required

scalar fields below must be present, and unknown top-level optimization keys

are rejected.

Set to false to skip Stage 35 while keeping the stage in the manifest

holdout_observations

Number of unique dates to reserve for the blocked holdout window

include_last_observations

Keep lag history for carryover-sensitive holdout scoring

coverage_levels

Coverage levels reported in Phase 10; use the fixed 50, 80, and 94 percent defaults

sampler

Optional validation-only sampler overrides for the train-window refit

Phase 10 reports coverage as coverage_50, coverage_80, and

coverage_94. Keep those defaults unless the implementation and tests are

updated together.

The validation stage builds a clean train-window model for holdout scoring and

ignores inference_data.path so the refit does not inherit attached posterior

state from Stage 00.

Override precedence

For the runner, precedence is:

Setting

Higher precedence

Lower precedence

Combined dataset path

dataset_path / --dataset-path

data.dataset_path