Posterior Predictive Checks

Use posterior predictive draws to check in-sample fit and to generate predictions for new rows that follow the fitted panel layout.

For diagnostic metrics after sampling, see Diagnostics. For table export, see Summary and Export.

Sample posterior predictive draws

Use PanelMMM.sample_posterior_predictive(...) on a fitted model:

sample_posterior_predictive(...):

- requires

X - uses the fitted posterior stored on

mmm.idata - reshapes

Xinto the model’s panel xarray layout - runs

pymc.sample_posterior_predictive(...) - returns an extracted

xarray.Dataset

By default, combined=True, so the returned dataset uses a sample

dimension. If you want separate chain and draw dimensions, set

combined=False.

Store or return only

By default, Abacus also writes the predictive samples back to mmm.idata:

With extend_idata=True, Abacus adds:

idata.posterior_predictiveidata.posterior_predictive_constant_data

If you only want the returned samples and do not want to update mmm.idata,

set extend_idata=False.

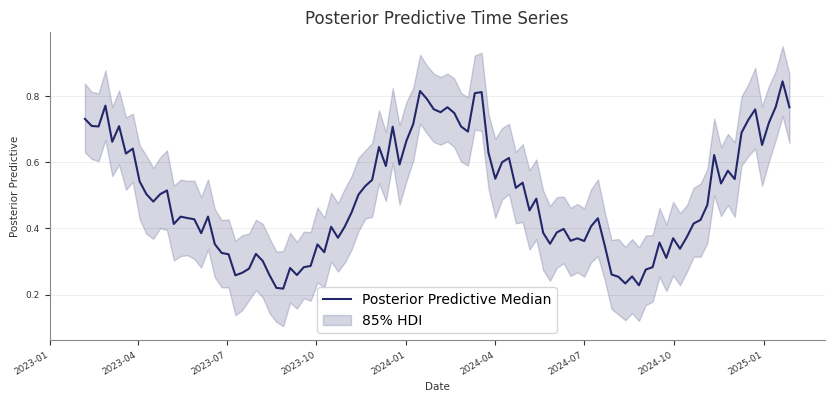

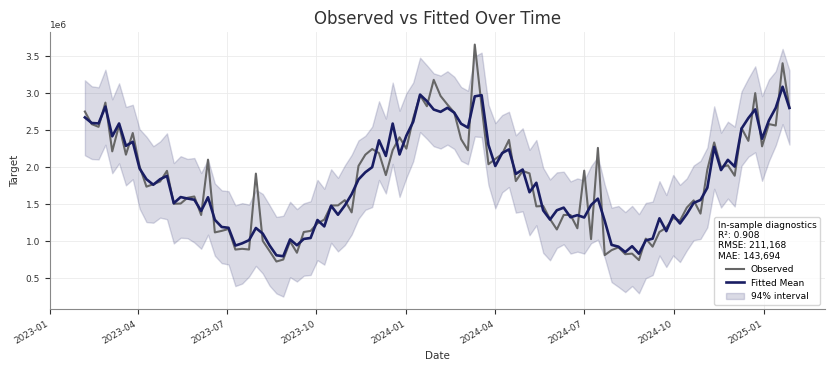

Check training-fit values against observed data

For an in-sample check, pass the same design matrix you used for fitting. This is the same pattern used by the pipeline’s Stage 30 training-fit assessment:

Example posterior predictive output:

mmm.summary.posterior_predictive() returns a table with:

- observed target values

- posterior predictive mean and median

- HDI bound columns such as

abs_error_94_lowerandabs_error_94_upper

You can also access the predictive draws directly:

Blocked holdout validation

For the structured pipeline’s Stage 35 validation, Abacus fits a fresh model on the training window and then scores only the holdout dates:

That holdout path is different from the in-sample check above:

- the model is fit on

X_trainandy_trainonly - the holdout

Xcontains only future dates include_last_observations=Truekeeps lag history for adstock carryover- the returned samples are used to compute holdout metrics such as RMSE, MAE, NRMSE, NMAE, CRPS, bias, and coverage at 50%, 80%, and 94%

The holdout stage is more expensive than the in-sample check because it adds a second fit.

Predict on new dates

For future prediction, pass a new X with the same structural columns as the

training data:

sample_posterior_predictive(...) does not take y. For a holdout or future

window, keep the actual target outside the model and align it yourself if you

want external evaluation.

Use include_last_observations correctly

Set include_last_observations=True when the forecast window needs lag history

for adstock carryover.

When enabled, Abacus:

- prepends the last

adstock.l_maxtraining observations internally - samples posterior predictive values on the padded data

- removes the prepended rows from the returned result

This only works when the input dates do not overlap with the training dates.

If they do overlap, Abacus raises a ValueError.

Practical guidance

- Use the training

Xfor fitted-versus-observed checks. - Use future-only dates for forward prediction.

- Use the training-window refit pattern for blocked holdout validation.

- Keep

combined=Trueif you want a simplersampledimension. - Use

combined=Falseif you need explicitchainanddrawdimensions. - Call

sample_posterior_predictive(...)before usingmmm.diagnostics.predictive_summary()ormmm.summary.posterior_predictive().

Common pitfalls

- Calling

sample_posterior_predictive(...)withoutX - Expecting

yto be passed into the predictive method - Using

include_last_observations=Trueon dates that overlap with training data - Forgetting that the returned object is extracted samples, while the stored

idata.posterior_predictivegroup keeps the native posterior predictive structure